Estimated reading time: 6 minutes

In residential real estate development projects historical land price risk plays an important role. Land price is defined as the difference between the market value of the property and its construction costs1 ; it is also known as the residual value. It represents the additional value over the construction cost of the property. It is the add-on that people are willing, or are able, to pay to live in a certain area.

As property prices and construction costs change due to market forces, the residual land value can become quite volatile. This represents an important risk factor for landowners andland developersas their result largely depend on changes in these residual values.

Key questions for land and project developers are therefore:

- How much did land prices change historically ?

- What is the land price risk in the current environment?

- How reliable is the risk estimate?

To answer these questions, we start with an historical overview of land prices since 1914. Next, we create context-dependent risk estimates using a regime-based risk model. We measure the reliability of the estimation by performing out-of-sample backtests and compare the performance to a standard risk model. Finally we discuss the implications for land owners.

Land price history: more than one century of data

As land prices can be obtained as the difference between market property prices and construction prices, we can reconstruct the historical residential land price from these two components.

The graph below shows both new house prices, construction costs and the derived land prices since 1914 for an average house in the Netherlands:

We observe that average new home prices have increased significantly over the last century, from 11k to 501k, or with 3.6% (CAGR) per year. Construction costs have increased to 308k. By the end of 2023 the average residential residual land value in the Netherlands was therefore 193k, or 38.5% of the total market price.

Land price movements are not constant over time. In addition, we note that the dynamics become cyclical. For longer projection horizons which we typical observe in development projects, this therefore leads to larger increases and decreases. The graph below presents the 4-year look-back percentual changes of land prices.

We clearly observe alternating cycles: 6 periods with increasing land prices and 6 periods with decreasing land prices. The dashed line shows that in 20% of the years land prices decreased with more than 42% over a 4-year horizon. However, the graph also shows 4 periods with land price decreases up to -100%: both World Wars, the ‘70s and the ‘80s. In these periods construction costs increased much more than property prices, which led to falling land prices.

Regime-based land price risk estimation

As land price risk depends substantially on the macro-economic context, we want to take relevant drivers into account when we make risk estimations. A regime-based risk model2 based onreference class forecasting principles helps us to achieve that. We first identify the macro-economic and other drivers like housing shortage that best explain land price movements. Next, for every observed year we select reference classes (years) whereby the (macro-economic) context is most comparable.

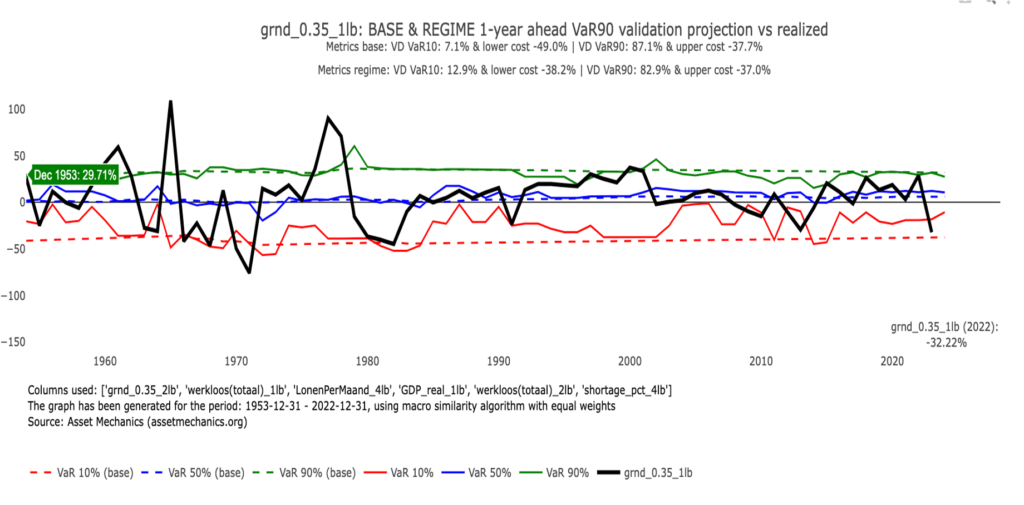

When we apply a walk-forward validation over the last 70 years we obtain the following back-test results for a 1-year horizon forecast:

We observe that the regime-based model is much more accurate and adaptable than a standard historical risk model. Furthermore, the regime-based model adapts better to changing regimes as can be seen by lower model costs. The regime-model is on average less conservative and more agile. Therefore we become more resilient in changing environments, which enables better decision-making.

Validations on holdout set

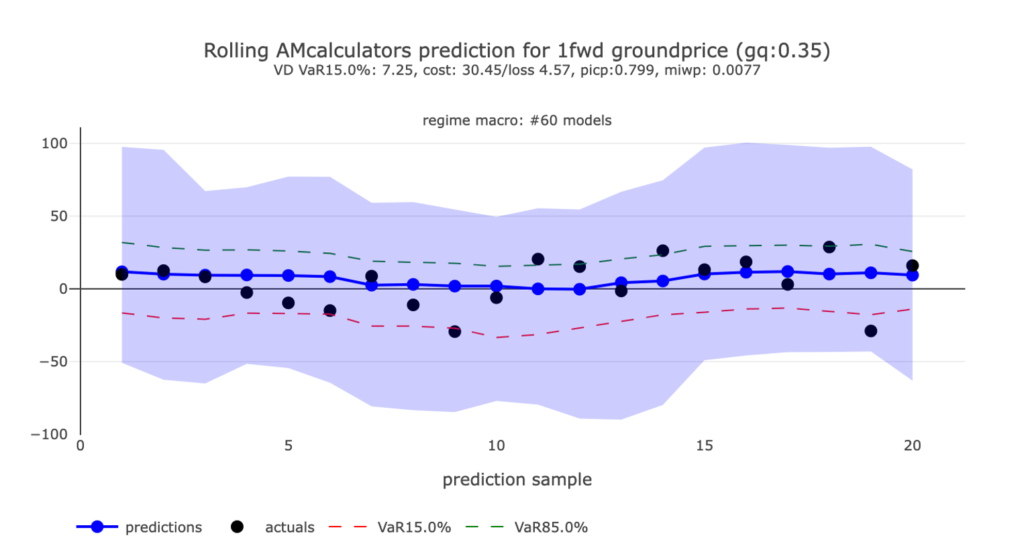

In addition we have also validated a combined set of best models on a holdout-set over the last 20 years. We found the following results:

It is good to see such a strong confirmation that our model works properly on unseen data over the last 20 years.

Implications for landowners

The historical analysis shows that land price risk can sometimes be very high. Accurate risk measurement therefore becomes imperative for landowners. However, it is not a trivial task. Depending on the selected method (e.g. base or regime), the resulting risk estimates can differ substantially.

Applying the base method is relatively simple. It would undoubtably simplify risk reporting; however, it leads to overestimation of risk in most of the years. This implies buffers that tend to be large even in low-risk periods that do not require so. We can confidently say that using a standard method comes with a high cost.

Employing a regime-based method, on the other hand, requires more careful consideration of the relevant drivers that might be relevant. However, when we do we can obtain a dynamic assessment of the risk environment, optimal decision making and buffer allocations. Risk metrics will now much better guide us to know when a project should be continued, to be put on hold or to be stopped entirely.

So, what does the future hold? Although we do not know the exact direction of land prices, we already have a much clearer and more robust view of the magnitude of the risks. This helps us a lot to be more agile in our decision making and to substantiate our decisions with data. Reach out for a free consultation on risk mapping and measurement within your organization. Or see how this model can be used to obtain a complete overview of the risks with the land development risk tool.

- Construction costs including VAT and profit margin for the contractor / project developer ↩︎

- We apply an ‘optimized (multivariable) similarity-based risk model’. The Regime-Simple model selects the most relevant features from the observed variable itself and captures the business-cycle risk. The Regime-Macro model also includes other relevant macro-economic and business variables. The models are optimized out-of-sample to obtain the most robust forecast of the risk. ↩︎